Americans are paying more for consumer goods during the biggest surge in U.S. inflation in more than 30 years.

Header Image: Forbes

Americans across the country are seeing higher prices at grocery stores and gas stations, causing even more pain for their wallets and pocketbooks right as the holiday shopping season is set to commence.

Data released by the Labor Department earlier this week indicates inflation has risen at its highest rate in over three decades. Consumer prices soared by 6.2 percent compared to the same period last year. This is the biggest one-year jump seen in the government’s consumer price index since 1990.

The increase in prices is surpassing wage gains and forcing Americans to dedicate a bigger share of their income to necessities such as food and gas. In particular, according to the Bureau of Labor Statistics data: meat, chicken, dairy, eggs, sugar and coffee are among the products that have seen especially large price gains in the past year.

Additionally, in the past year, energy costs have jumped a stunning 30 percent, with gasoline soaring by nearly 50 percent. A gallon of gas, on average, was $3.42 nationwide on Tuesday, according to AAA — up from $2.11 a year ago. The energy index climbed by some 4.8 percent last month alone and the gasoline index gained 6.1 percent. This marks the fifth consecutive monthly increase in gasoline prices.

Prices for natural gas and heating oil are also on the rise. For instance, the Energy Information Administration has predicted that Americans could spend up to 30 percent more on natural gas and 43 percent more on heating oil this coming winter.

Economists predict high inflation will subside sometime next year once the widespread shortages of supply and labor begin to ease, but it’s very unclear how much or how quickly price pressures will fade. In the meantime, inflation will continue to eat up American households in terms of consumer spending.

Chairman of the Federal Reserve Jerome Powell listens during a hearing before the Senate Banking Committee in December 2020.

On Tuesday, Feb. 23 at 11 a.m. EST, the chair of the Federal Reserve, Jerome Powell, testified before the Senate Banking Committee regarding the central bank’s semi-annual Monetary Policy Report. The Committee’s chair, Senator Sherrod Brown (D-OH) began the session with opening remarks about the current state of economic affairs. Senator Brown made it clear from the beginning that he is in favor of the Fed using any monetary tools it sees fit to manage inflation and unemployment, stating, “most people are not worried about doing too much to get through this pandemic, they’re worried about doing too little.” Further, he recalled remarks from Janet Yellen, the treasury secretary, who stated that if the Fed doesn’t do more by way of monetary policy, we risk a “permanent scarring” of our economy and our future.

Ranking member Senator Pat Toomey (R-PA) disagreed with Senator Brown, stating, “the last thing we need is a massive multimillion-dollar spending bill.” Senator Toomey was chiefly concerned with inflation and urged Powell to roll back the Fed’s holdings of treasury securities and agency mortgage-backed securities in order to avoid uncontrollable and unwanted inflation. Senator Toomey stated that most American households are in better financial positions now than they were before the pandemic. He stated that in his opinion, the last two recessions were caused by asset bubbles that burst. In 2001, it was the stock market, in 2008, the mortgage credit market. Additionally, Senator Toomey believes that monetary policy contributed a great deal to the formation of those bubbles.

He also remarked that there is a link between record amounts of liquidity and unprecedented asset valuations, like those of GameStop and Bitcoin, as of late. Across the board, Senator Toomey stated, there are elevated asset prices and signs of emerging inflation. He asked Powell if he believes there is a link between the liquidity the Fed has been providing and some of these unprecedented asset prices, to which Powell responded, “there is certainly a link.” Despite this, Powell and the Fed plan to continue the bond-buying program “at least at its current pace until we make substantial progress toward our current goals.”

Powell presented his testimony in two parts: a review of the current economic situation and the Fed’s plans for monetary policy moving forward. Powell stated that the sectors most adversely affected by the resurgence of the virus are the weakest. Household spending on services remains low, especially in the hard-hit sectors of leisure and hospitality. However, household spending on goods picked up in January. Moreover, the housing sector has “more than fully recovered from the downturn.” Regarding the labor market, Powell stated that the pace of improvement in the labor market has slowed and the unemployment rate remained elevated at 6.8 percent in January. Participation in the labor market is notably below pre-pandemic levels.

Moreover, Powell stated that “those least able to shoulder the burden [of the pandemic] have been hardest hit,” citing low wage workers, African Americans, Hispanics and other minority groups as the most affected. During the questioning portion of the hearing, Senator Bob Menendez (D-NJ) explained the varying unemployment rates by race: in January, the unemployment rate among the black population was 9.2 percent; among Hispanics, 8.6 percent. The unemployment rate among white people was 5.7 percent. Additionally, the Black labor force exit rate increased dramatically while the white labor force exit rate returned to pre-pandemic levels, suggesting that the Black unemployment rate is misleadingly low compared to the white rate. Senator Menendez got Powell to agree that minority families are bearing the brunt of the damage caused by the pandemic, “along with those at the lower end of the income spectrum.”

Regarding inflation, Powell stated that there were large declines in the spring, but consumer prices partially rebounded last year. Powell also stated that as the very low inflation readings from last March and April drop out of the 12-month calculation on inflation, we should expect readings on inflation to move up. This is called the base effect and it should not be a cause for concern. Powell mentioned that overall, inflation remains below the 2 percent long-run objective. He stressed that the 2 percent goal is an average, so periods of lower-than-average inflation should be followed by periods with inflation rates greater than 2 percent.

In his overview of the monetary policy report, Powell emphasized that maximum employment is a broad and inclusive goal, so policy decisions should be informed by an assessment of the shortfalls of employment from its maximum level, rather than deviations from its maximum level. Furthermore, Powell mentioned that actions taken by the Fed in the early months of the pandemic have constrained their main policy tool by the lower bound. In other words, the Fed has been lowering interest rates in unprecedented ways since even before the start of the pandemic, so their ability to use lowering interest rates as a monetary policy tool is weakened.

If lowering interest rates isn’t really much of an option anymore, what will the Fed do? Simply put, the Fed will do what it has been doing throughout the pandemic: increase holdings of securities at least at their current pace. The Fed will closely monitor inflation; Powell stated that “well-anchored inflation expectations will enhance our ability to meet both our employment and inflation goals.” Powell assured Congress that the Fed “will continue to clearly communicate our assessment of progress toward our goals well in advance of any change in the pace of purchases.”

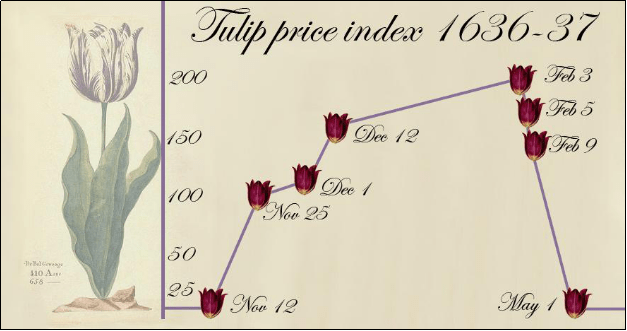

Pictured above is the price index of Tulips from the infamous Tulip bubble burst of the 1600s in the Dutch Netherlands. The tulip bubble burst is the first ever recorded financial bubble in history.

Chances are if you checked the financial markets on Tuesday morning, indices were in the red. Many investors were concerned with a large federal stimulus package, the recent rise in commodities, and a rise in the 10-year U.S. Treasury Bond. Headlines regarding Michael Burry’s prediction about hyperinflation, Treasury Bonds, and WTI Crude Oil exploding to over $60 a barrel flooded the news on Monday and investors were alarmed. Tuesday’s open saw the tech heavy NASDAQ dropping nearly 3 percent.

Amid growing concerns among investors, talks of a potential financial bubble, which occurs when asset prices become based on inconsistent and irrational views about the future, surfaced and Ray Dalio’s bubble indicator found 50 of the 1,000 biggest companies are in extreme bubbles. Although this is only half of the companies considered in a bubble from the Dot Com burst, investors should certainly take notice but not let news headlines deter from their equity investing.

Nonetheless, financial bubbles and investor psychology is still a fascinating topic. I recently became interested in the concept of financial bubbles after picking up a copy of the novel, Irrational Exuberance by Economist J.D. Shiller. In his book, Shiller accurately predicted the housing crisis and suggests monetary policy tools to ease the consequences of financial bubbles. The term “Irrational Exuberance” was coined by former Fed Chairman, Alan Greenspan, in the late 1980s. Below is the breakdown and examination of the history of bubbles.

Financial bubbles have occurred all throughout history; In the 1630s, the Dutch went crazy for Tulip bulbs. The price soared from 1636 to 1637 and many went so far as selling their homes to purchase the simple garden plant. Eventually, the mass hysteria surrounding tulips faded and the price of tulips declined 90 percent..

Do you remember Isaac Newton, the pioneer of the concept of gravity? Well, Newton was burned hard and lost a fortune when the South Sea Company bubble burst in the 1720s. The South Sea Company was promised a monopoly by the British government to trade in South American colonies. British investors dived headfirst into the South Sea and the stock reached a high over 1,000 pounds and then came down after news of fraud and the monopoly fell out.

Bubbles are no phenomena to the past as we have seen in the modern era. The Japanese real estate and equity markets exploded in the late 1980s and then came down. The Dotcom bubble occurred in the United States in the late 1990s to early 2000s when investors dived into tech and internet stocks. The most recent bubble occurred with the U.S. housing market in the late 2000s to 2010s. Housing prices increased dramatically leading many investors to falsely believe the inability of the housing market to crash. The market declined dramatically, due to an excess of subprime mortgage loans, followed by the global recession due to mortgage securitization.

History certainly has a knack of repeating itself and we could be seeing another bubble occur in any sector of the economy. With bubbles and investor mania creating a collapse of asset prices, the key to surviving the next bubble is to rely less on weekend worrying, where we, as retail investors or institutional investors, absorb weekly news on the weekend leading to a belief in an economic doom at the start of a new week. To take from Peter Lynch, we should not get scared out of stocks.